The first quarter reminded investors how quickly the macro backdrop can shift. As conflict in Iran disrupted energy markets and stress spread through private credit, warnings of a 1970's style stagflation environment resurfaced and sent markets into a tailspin.

At a Glance:

• War in Iran sets the tone and geopolitics quickly overwhelm early‑year optimism.

• Brent surges past $100 as risks to the Strait of Hormuz ignite inflation fears.

• Private Credit redemptions grow as investors pull money from illiquid private credit funds

• Equities lose momentum after a strong start as sentiment turns risk‑off.

• Bonds reverse early gains: yields rise as inflation expectations increase.

• Rate‑cut hopes fade; markets shift from expecting Fed easing to fearing hikes, due to the inflation pressure from the oil shock.

• Investment Ideas: Inflation Protected Bonds, Long Short Hedge Funds, Fallen Angel - Microsoft

The first quarter of 2026 clearly marked a decisive shift in market sentiment. Following years of very strong returns, investor optimism quickly faded as the war in Iran pushed oil prices sharply higher and revived inflation concerns.

At the same time, rising redemptions across a number of private credit funds highlighted the vulnerabilities of illiquid strategies after years of excess liquidity and easy financial conditions, or as Warren Buffett once observed, “Only when the tide goes out do you discover who’s been swimming naked.”

The most acute concern for investors emerged from the sharp rise in oil prices with energy once again acting as the transmission channel to higher inflation. Brent crude oil moved decisively above $100 per barrel, as shipping in the Strait of Hormuz, a critical artery that handles 20% of global oil and gas supply, came to a standstill. Even the International Energy Agency (IEA) warned that this has the potential to be a bigger shock than the two oil shocks in the 1970’s combined.

Impact on financial markets

The reaction across financial markets has been swift. Global equities, which started the year well, fell 7% in March, and are now down 3% for the year. Bonds initially rallied on flight to safety concerns but subsequently sold off (-3.1%) on inflation fears. The US dollar rallied while Commodities soared (+23.8% ytd). Even Gold failed to provide safety, falling 11% in March, but it remains among the best performing assets year to date, up 8.6%.

Monetary Policy Expectations Reset

The key question facing investors now is; is this oil shock something that will end this cycle and trigger a recession? Obviously, no one knows how long the war will last, or how quickly other sources of oil can come on stream, but the risk is not insignificant.

But the war comes at a time when the jobs market is also showing signs of fatigue with 94k jobs lost in the US in February.

Prior to the war, expectations had pointed to 25–50 basis points of rate cuts from the Federal Reserve and other major central banks as inflation continued to cool. Renewed inflation pressure has prompted economists and policymakers to warn that rate cuts could be delayed, be smaller in magnitude, or even increase.

Redemptions in private credit funds accelerate

Jamie Dimon’s warning last year about “cockroaches” lurking in private credit was widely dismissed as colourful exaggeration. It feels less so today. Private Credit manager Blue Owl’s move to limit withdrawals from one of its funds is an unmistakable sign of stress. So, too, is Blackstone’s decision to allow redemptions of nearly 8 per cent from its flagship BCRED fund. Research from UBS indicating that private credit default rates could approach mid teens levels in a tail risk scenario, adds unwelcome perspective.

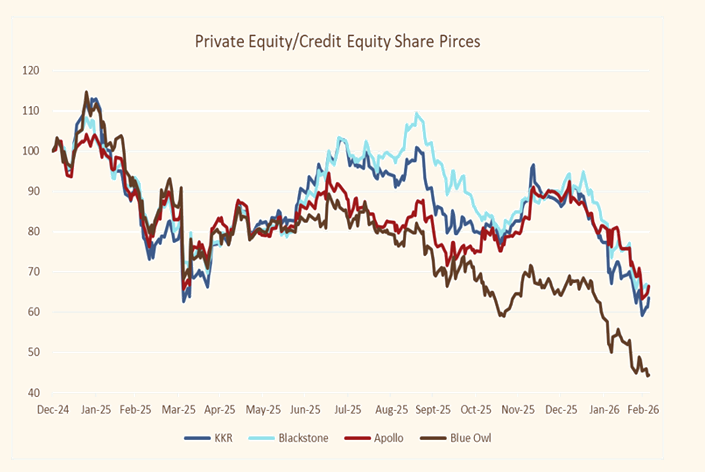

Is the Equity market the ‘canary in the coal mine’ for private credit?

The public equity market has already delivered its judgement. Listed private equity and alternative lending groups have seen their share prices fall 30 to 50 per cent in recent months, reflecting expectations of further redemptions, and rising balance sheet pressures. Equity markets are forward looking, and the scale of these drawdowns suggests that equity investors believe the private credit adjustment is only in its early stages.

Figure 1: Private Asset firms share prices

Investors should focus on Investment Grade

Our view entering the year, that credit markets were priced for near perfection and that investors should prioritise balance sheet strength, liquidity and income over capital gain potential, has not changed. In this environment, investment grade credit remains the most reliable anchor. IG issuers offer solid carry, strong liquidity and robust fundamentals, the characteristics that matter most when volatility picks up.

Outlook for the rest of 2026

As Warren Buffett observed, “Only when the tide goes out do you discover who’s been swimming naked”.

We think the recent pullback serves as a timely reminder that portfolios should be built not just to perform in good times, but to endure when conditions turn.

The Equity market has enjoyed a stellar run in recent years, but periods of adjustment have a habit of exposing leverage, liquidity mismatches and optimistic assumptions that were easier to ignore when money was cheap and volatility suppressed. We think events in the frist quarter serve as a timely reminder that portfolios shold not just be built for the good times, but shold also be built to endure the bad.

Portfolio positioning for more challenging times

What does this mean?

• In Equities rather than taking a fully “risk on” or “risk off” approach, we favour a more balanced allocation that combines selective growth opportunities and leaning into more defensive structural themes with durable earnings, from infrastructure, cybersecurity, healthcare to defence.

• In Fixed Income, we continue to focus on the safer parts of the market for downside protection should global growth slow. Within sovereign bonds we continue to advocate shorter duration positions as inflation pressures persists, while in credit we continue to prefer the liquid investment grade corporate credit exposure, while inflation protected securities help guard against the risk that inflation pressures re-emerge.

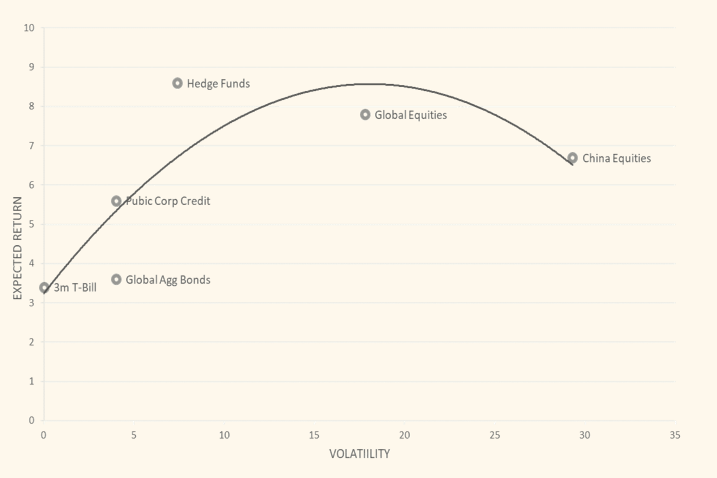

Hedge Funds: Higher return with lower Risk?

Looking ahead we think that markets are likely to be more selective, and the strategies that outperform will be those that can identify mispricing, adapt quickly, and capture opportunities beyond the traditional long only framework.

We think Hedge funds, long-short funds in particular, play a crucial role in this new investment regime. Their ability to generate returns from differentiated sources, many of which are not accessible in traditional portfolios, makes them uniquely well-suited to today’s environment.

Figure 3. illustrates the point, with the latest Blackrock Capital Market assumptions predicting that over the next 5-10 years Hedge Funds are expected to deliver higher returns than equities but with lower volatility. By integrating carefully selected hedge fund strategies, we aim to enhance diversification, reduce volatility, improve risk adjusted returns.

Figure 3: Hedge Funds expected to deliver higher returns with lower volatility.

Inflation protection via TIPs

Similarly. with the changing inflation landscape adding to inflation protection bonds or ‘TIPS’ as they are commonly known seems prudent. Treasury Inflation Protected Securities (TIPS) are government bonds designed to help protect investors from rising inflation.

Unlike conventional bonds, where the principal value is fixed, the principal of a TIPS bond increases in line with changes in the consumer price index (CPI) and falls if inflation declines. For portfolios, TIPS can provide real, inflation adjusted income while preserving purchasing power in periods when traditional fixed rate bonds may struggle.

Fallen Angel - Microsoft

For investors with a longer term time horizon, and for those who can withstand the volatility, opportunities are beginning to emerge.

Microsoft, for example, has been impacted by broader market weakness and a degree of “AI fatigue,” and its share price has declined by approximately 33% from its peak last November. A materially larger drawdown than many other large AI exposed technology companies have experienced.

Following this correction, Microsoft’s valuation has become considerably more attractive. On a forward earnings basis, the stock now trades broadly in line with the U.S. market average at around 21x earnings, despite analysts’ expectations that Microsoft’s earnings growth will be roughly double that of the broader market.

While market volatility may persist over the near term, such periods often create opportunities to build or add to long term core holdings and high quality companies like Microsoft are increasingly offering entry points that were not available during the peak of market enthusiasm.

If you would like to explore any of the themes discussed, or to review how your portfolio is positioned considering current conditions, we would be pleased to discuss this with you. Please do not hesitate to contact a member of the Typhoon Capital team.