Policy Tailwinds and AI Keep Growth on Track

Global markets have begun the year on a positive note. Surveying the forecasts emanating from Wall Street, the outlook for 2026 is easily condensed into a tidy equation: AI investment plus looser fiscal and monetary policy equals growth.

The numbers lend this consensus view a degree of credibility. Economists expect world growth to remain close to its long run trend of about 3 per cent. But the familiar “three speed” pattern across regions persists.

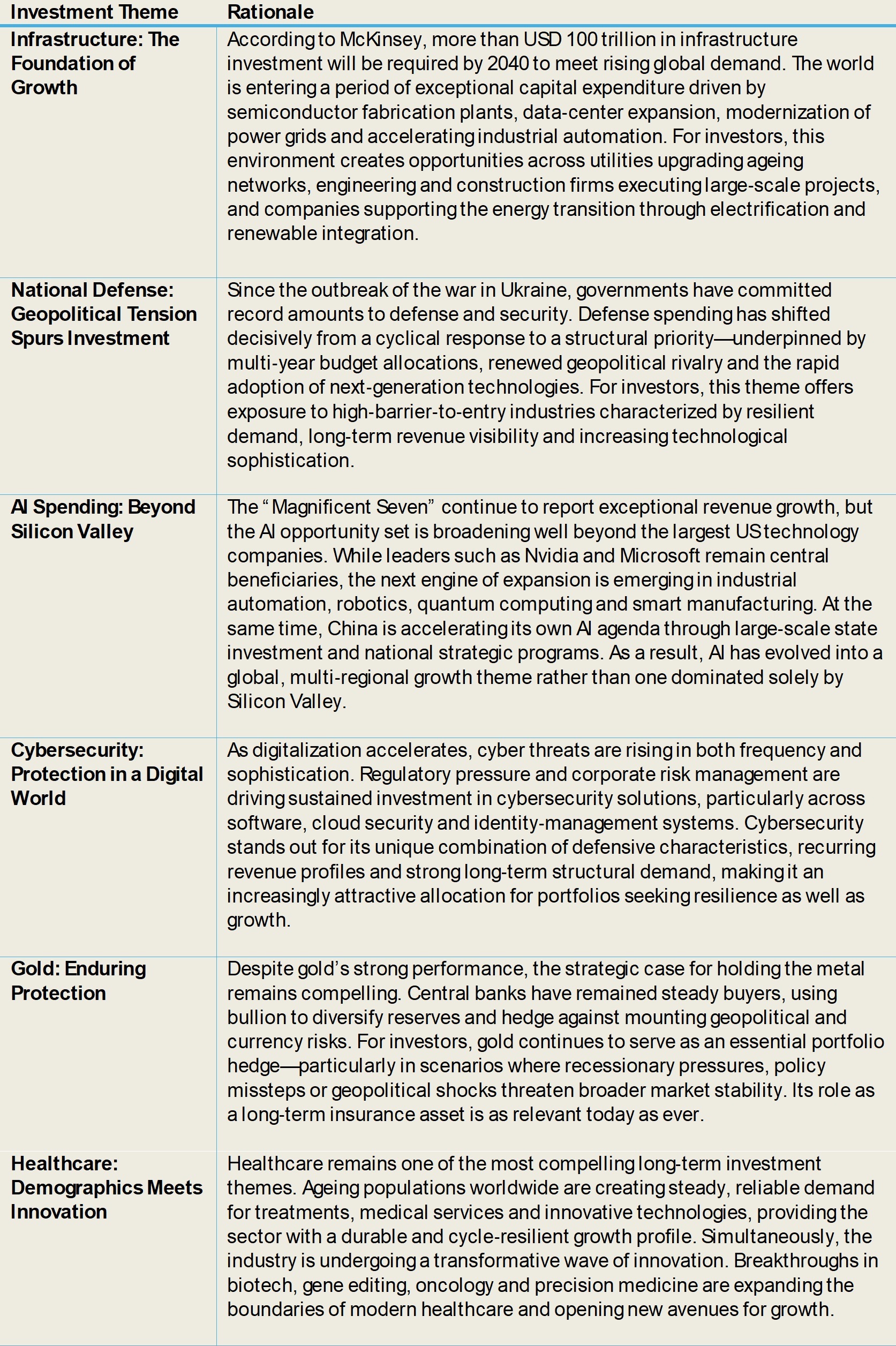

The US economy is forecast to expand by 2.1 per cent, propelled by resilient consumer spending and investment. Europe, by contrast, is set for another subdued year, with growth estimated at just 1.2 per cent. China, meanwhile, is expected to grow by around 4.5 per cent as policymakers strive to stabilise activity and support confidence (Figure 1).

Figure 1: Global Economic Forecasts, 2026E

The 2026 Investment Playbook

So, what does this mean for investors? Unsurprisingly, this positive economic backdrop sets the tone for 2026. Corporate earnings are forecast to rise by about 10%, marking a further year of solid profit growth. Yet the environment facing investors has become more nuanced, shaped by concerns about US valuations and a shifting global currency landscape as the dollar shows weakens.

In this context, the investment approach going forward is clear. The AI fuelled capital expenditure boom remains the main growth engine, and investors would be unwise to abandon it.

But the maturing of this cycle argues for more diversification across assets and themes in a portfolio context. That means spreading positions across asset classes, favouring the sturdier corners of the fixed income market; shifting some equity exposure towards regions were valuations that still offer value; and leaning into structural themes with durable earnings, from infrastructure, cybersecurity, healthcare to defence. A weakening dollar also makes a more diversified currency mix prudent.

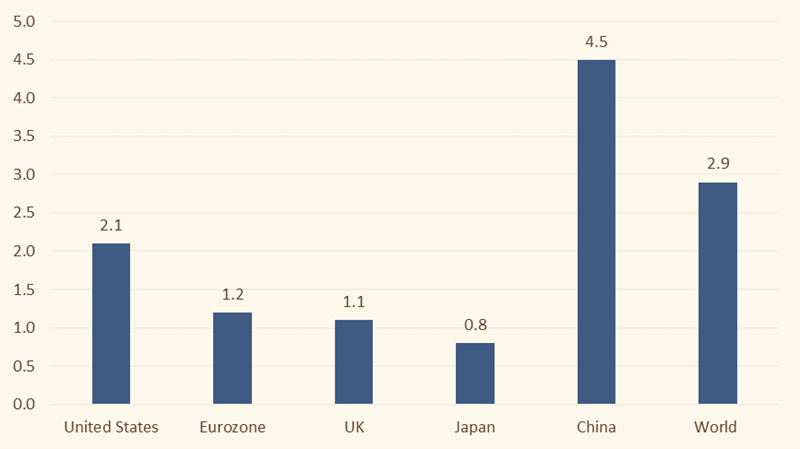

Figure 2: Investment Ideas for 2026

Equities: From Concentration to Diversification

The central force in global equity markets remains AI, but focus is beginning to broaden beyond Silicon Valley. The next stage is likely to favour companies tied to the infrastructure underpinning AI adoption and the energy transition, from electricity grids and power system upgrades to industrial automation and advanced manufacturing. These areas stand to benefit from sustained investment as energy demand shifts to renewables and companies modernise production.

At the same time, valuation gaps across regions are becoming harder to ignore. With US equities trading at elevated multiples and the prospect of a softer dollar, Europe, Japan and China present credible alternatives to investors.

Longer term structural themes also continue to offer investors good opportunities. Cybersecurity, infrastructure, healthcare and defence are attracting persistent capital flows as governments and companies prioritise resilience in an increasingly complex geopolitical environment.

Fixed Income: A Premium on Quality

In a world where the trajectory of interest rates is lower (outside of Japan) bonds retain their value for both yield and protection. Yields remain attractive by historical standards, and fixed income continues to offer a valuable counterbalance to potential equity volatility. The emphasis, however, is firmly on quality.

In the U.S., political pressure on the Federal Reserve to cut rates is mounting. The likely outcome is a modest steepening of yield curves. Rate cuts should compress the front end, while fiscal dynamics and structural investment needs, such as AI infrastructure and the energy transition, keep long yields supported. Short dated government bonds provide both appealing income and reliable downside protection.

Credit markets, however, present a more nuanced picture. Valuations are stretched as evidenced by tight credit spreads, and comments from the likes of Jamie Dimon warning about “cockroaches” lurking in private credit underscore the need for caution. Investors should prioritise investment grade issuers with robust balance sheets, and credit should be viewed primarily as an income sleeve, not a source of capital gains from further spread compression.

FX: Dollar Likely to Remain Under Pressure

The US dollar ended last year as one of the more notable laggards. The policy mix emerging from President Trump’s “Make America Great Again” agenda, combining deficit expansion, targeted tax incentives and a bias toward lower interest rates, points to potential further softness ahead.

With the Federal Reserve poised to continue easing, institutional forecasters see scope for the dollar to fall by 5 per cent, and potentially as much as 10 per cent, over the coming year. A weaker currency would not only align with Washington’s fiscal expansion objectives but also sit comfortably alongside the goal to make America competitive again.

Gold: A Steady Source of Insurance

Finally, despite its stellar run, with prices now above $4,500 an ounce, the fundamental reasons for holding Gold in a portfolio remains in-tact. Central banks have been persistent buyers, using the metal to diversify reserves and hedge against geopolitical and currency risks. For investors, a small holding of gold still makes sense in scenarios where recessionary pressures, policy missteps or geopolitical shocks threaten market stability.