Defence Spending: A New Strategic Era

Recent events in Iran have provided yet another, and unwelcome reminder, of how precarious the global order has become. In response to increased conflict governments worldwide are accelerating defence spending at a pace not seen since the Cold War, as geopolitical instability and strategic competition reshape fiscal priorities.

To put the spending into context, according to the Stockholm International Peace Research Institute (SIPRI), global military expenditure reached a record $2.7 trillion in 2024, marking a 9.4% increase from the previous year (Figure 1). This was the sharpest annual rise in over three decades. Military spending has now increased for ten consecutive years, climbing over a third since 2015.

Historical and Recent Trends in Defence Spending

Between 1990 and the early 2000s, many Western nations reduced their defence outlays, prioritising domestic spending and peacekeeping operations over large-scale military readiness. However, recently with rising geopolitical tensions, global military expenditure has increased. This resurgence has been driven by the growing recognition that strategic deterrence requires sustained investment. The trend is expected to continue as nations adapt to a more fragmented and contested global security environment.

Figure 1: Global Defence Expenditure; 2015-2025

NATO’s Strategic Pivot: From 2% to 5%

In a landmark shift, NATO Defence Ministers agreed in June 2025 to raise the alliance’s defence spending benchmark from 2% to 5% of GDP. The proposed breakdown includes 3.5% of GDP for core military needs, personnel, procurement, training, and modernization, and 1.5% of GDP for strategic investments in infrastructure, cybersecurity, intelligence, and resilience. This move reflects growing pressure from Washington to rebalance transatlantic burden-sharing.

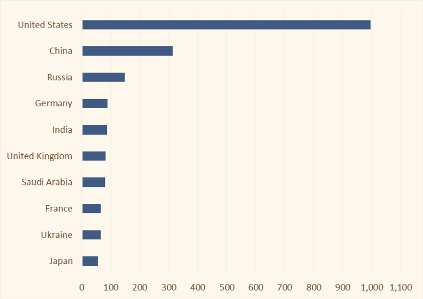

In a global context the United States remains the world’s largest defence spender, allocating $997 billion in 2024, equal to over one third of global military expenditure, more than three times the outlay of China, the next largest spender.

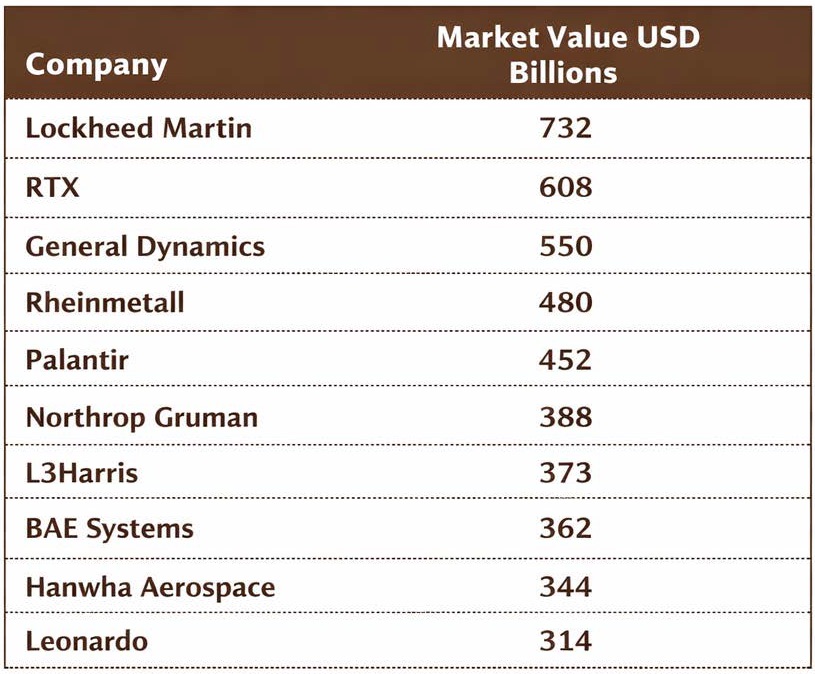

Washington’s dominance is underpinned by the scale its defence industrial base. The sector is led by a cluster of major contractors, Lockheed Martin, RTX, Northrop Grumman, General Dynamics, Boeing and L3Harris, which consistently occupy top positions in global rankings and collectively capture a substantial share of global arms revenue. (Figure 2)

Figure 2: Top 10 Defence Companies by Market Value

Europe increasing Expenditure

Europe is also stepping up. After years of underfunding EU member states have responded to Russia’s invasion of Ukraine with a marked increase in defence investment. EU-wide spending rose from €168bn in 2019 to €326bn in 2024, representing approximately 1.9% of GDP. While still below NATO’s benchmark, the upward trajectory signals a strategic shift.

Germany is now the fourth-largest defence spender allocating $84 billion (Figure 3). The EU’s Readiness 2030 initiative, which aims to mobilise €800 billion over five years, which will further stimulate domestic production and reduce reliance on non-European suppliers and boost demand for regional manufacturers such as BAE Systems, Thales, Leonardo, Rheinmetall, and Airbus, all ranked among the world’s top defence suppliers.

Figure 3: Top 10 Defence Spending Countries; in USD billion

Conclusion: A New Strategic Era

While the increase in global conflicts is an unwelcome development on many fronts not least the humanitarian suffering, the rise in defence spending marks a decisive shift in international priorities.

Yet the strategic implications are more complex. The rearmament trend risks entrenching rival blocs and escalating regional tensions. Policymakers must balance deterrence with diplomacy, and investment with integration.

From an investment perspective as governments recalibrate their security postures, the defence sector is poised for sustained growth. While the defence sector has benefited from these trends increased conflict will likely keep the sector supported for many years to come.