Credit Markets: Liquidity Keeps Its Nerve as Private Credit Blinks

Jamie Dimon’s warning last year about “cockroaches” lurking in private credit was widely dismissed as colourful exaggeration. It feels less exaggerated today with the sector remaining under pressure. Publicly listed Investment Grade credit in contrast continues to remain well anchored and provides investors with a more stable source of income in their portfolios.

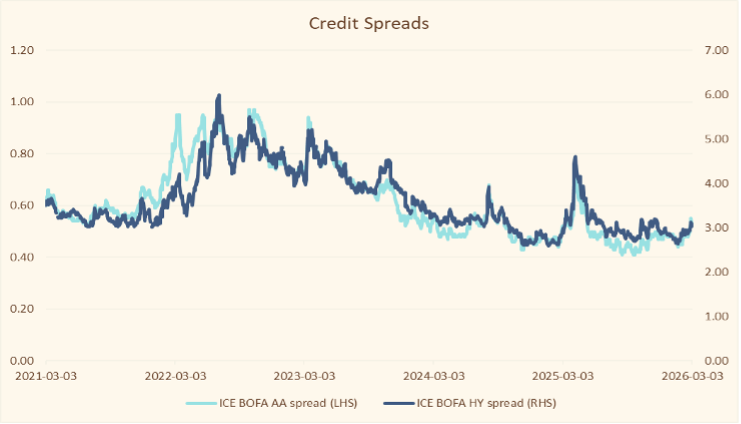

Liquid Credit remains stable

The US–Israeli strikes on Iran and subsequent retaliation lifted oil and safe haven demand, yet public, tradeable credit has remained orderly. In contrast, private credit faces mounting redemption pressure, governance questions and uncomfortable links to bank funding lines. The divergence is telling and it should shape portfolio choices.

Investment grade bonds have seen only a modest widening in spreads. IG remains anchored within a tight band of under 100 basis points over US Treasuries, which themselves continue to oscillate around the 4 per cent level as markets toggle between safe haven demand and rising inflation expectations. High yield, too, has held up better than many anticipated. With a heavy weighting in energy related issuers, HY spreads of roughly 300 basis points over Treasuries reflect a segment boosted — rather than threatened — by climbing oil prices.

This is the paradox of today’s public credit markets: the more liquid the segment, the less it appears disturbed by geopolitical escalation. Markets have absorbed higher oil, shifting rate expectations and a renewed bout of equity volatility without registering meaningful stress. In an environment where investors have spent years fretting about liquidity, it is the most liquid instruments that continue to display the greatest resilience.

Figure 1: Liquid Credit spreads remain tight

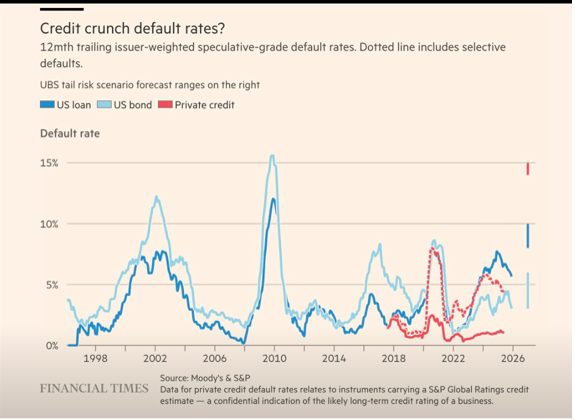

Private Credit remains under pressure

The same cannot be said for private credit, where cracks that were once easy to dismiss as idiosyncratic are becoming harder to ignore. What began as concerns around isolated borrowers has widened into a broader reassessment of the entire asset class.

Blue Owl’s move to limit withdrawals from one of its vehicles is an unmistakable sign of tension. So, too, is Blackstone’s decision to allow redemptions of nearly 8 per cent from its flagship BCRED fund — a figure that would have been unthinkable during the boom years of private credit fundraising.

More concerning is the growing list of lenders and credit lines now caught in the downdraft. A number of major financial institutions — including global banks and structured credit platforms — have been drawn into the spotlight as the failures of certain borrowers expose weaknesses in collateral structures and underwriting standards.

Research from UBS indicating that private credit default rates could approach mid teens levels in a tail risk scenario, roughly in line with historic sub investment grade high yield cycles, adds unwelcome perspective. It challenges the long standing narrative that private credit is inherently more insulated from volatility than public markets.

Figure 2: How much pain could private credit endure?

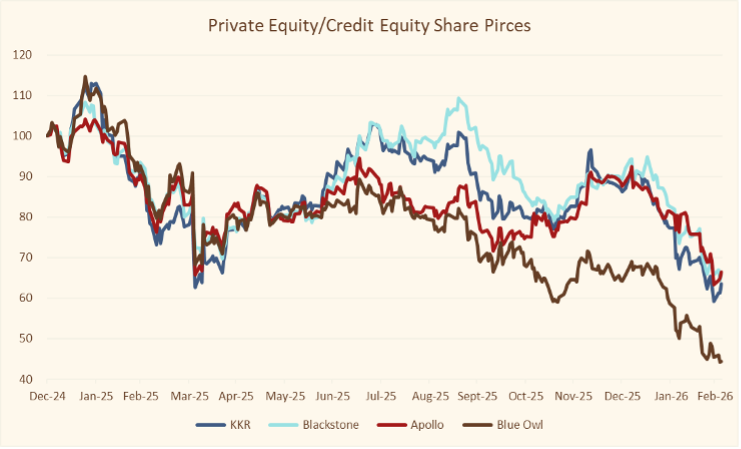

Is the Equity market the canary in the coal mine for private credit?

The public equity market has already delivered its judgement. Listed private equity and alternative lending groups have seen their share prices fall 30 to 50 per cent in recent months, reflecting expectations of further redemptions, liquidity constraints and rising balance sheet pressures. Equity markets are forward looking, and the scale of these drawdowns suggests that investors believe the private credit adjustment is only in its early stages.

Figure 3: Private Asset firms share prices

Our Views: Proceed with Caution

Our view entering the year, was that credit markets were priced for near perfection and that investors should prioritise balance sheet strength, liquidity and income over capital gain potential, has not changed.

In this environment, investment grade credit remains the most reliable anchor. IG issuers offer solid carry, strong liquidity and robust fundamentals, the characteristics that matter most when volatility picks up. High yield can still play a role, but only with careful issuer selection. Private credit, by contrast, demands patience. Until redemption pressures ease and transparency improves, discretion is not just prudent it is necessary.